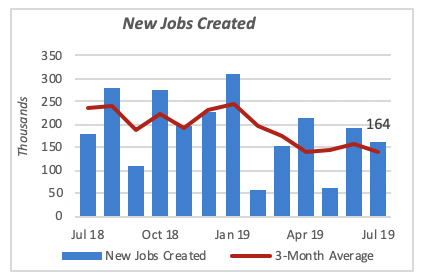

Jobs, jobs, jobs.

While the number of new jobs created in July was relatively strong, it’s lower than the monthly average of 194 thousand created in the preceding twelve months. In fact, the 164 thousand new jobs for July is just about equal to the average number for the first half of this year.

The US growth machine has slowed down however. Year to date through July 1.16 million jobs have been added to the employment rolls, 27% less or 433K fewer, than the 1.59 million jobs created in the same period last year.

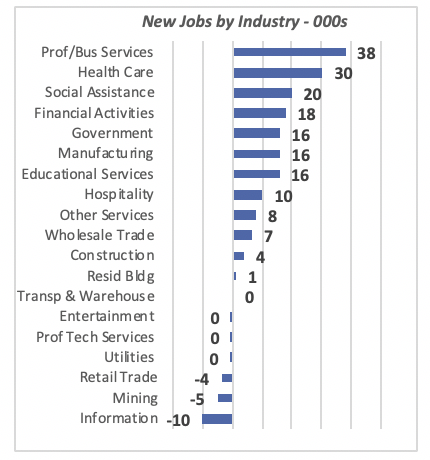

The leading areas in job creation last month follow the same pattern of previous months; Professional & Business Services leads with the largest number of new jobs accounting for over one fifth of the total. Health Care contributed 30 thousand news jobs, just under one-fifth of July’s total.

At the other end we can see that Information lost ten thousand jobs in the month, while Mining and Retail Trade also lost, five and fourth thousand jobs each, respectively.

The Manufacturing sector added one in ten of July’s new jobs, or 16 thousand jobs. But year-to-date manufacturing industries have added only 55 thousand jobs, about a third of those added in the same period last year.

Overall job growth for the next few months will be bolstered through hiring by the Census bureau, that will need around 750 thousand workers to assist in taking the 2020 Census. For the 2010 Census, the bureau hired approximately 635 thousand persons.

Other positive news on employment were Hourly Wages, which have been rising at a 3.3% annual rate. Retail Trade and Information sectors had the highest wage growth over the last year, at 4.5% and 5.8% year each, respectively. Paradoxically, employment in both of these sectors has fallen year-to-date compared to last year. But their average wage increase may be the mathematical result of substituting machines for workers, that is, you eliminate lower paying jobs from the calculation and the average automatically increases.

Labor Participation also improved in July. The rate rose one-tenth to 63%; although higher than a year ago it lags the beginning year rate that was at 63.2%.

But the number of weekly hours worked fell by one-tenth to 34.3 hours. Biggest reductions in hours worked were in Utilities (down seven-tenths of an hour or 1.6%), Transportation & Warehousing (three-tenths or 0.8%) and Manufacturing seven-tenths and 1.5%).

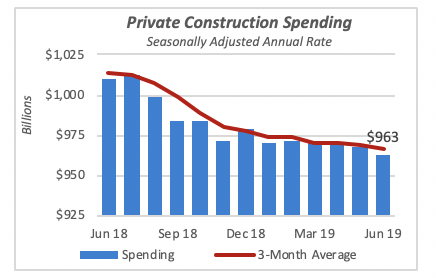

Construction sector is also weak, and weakening

The construction sector continues to weaken. Total spending for private construction projects declined by four-tenths of a percent (0.4%) in July to $963 billion. This drop comes on the heels of a three-tenths of a percent decline the previous month. In fact, the chart below clearly shows the declining rate of construction spending over the last year.

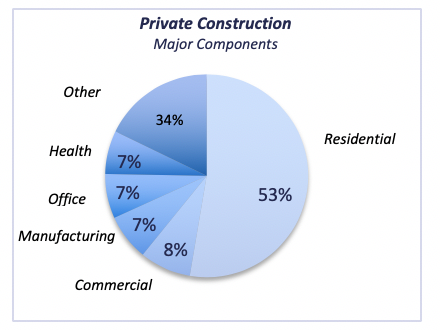

Private construction spending is nearly equally divided between residential projects, 53% of the total, and non-residential with the other 47% of spending.

Commercial construction includes all types of retail establishments such as stores and home centers, as well as supermarkets and food stores. Restaurants and bars fall within this category.

The Other category in the pie chart above includes a variety of projects such as Amusement & Recreation structures, Religious, Education, etc.

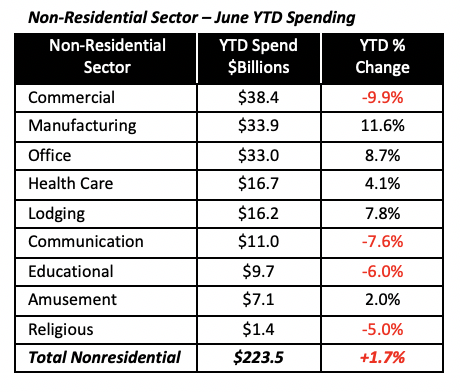

Private construction is running below last year mainly due to sharp declines in the residential sector. Year to date through June, residential spending is nearly 8% below the same period last year. In contrast non-residential is ahead by a modest 1.7%. One reason for the latter’s apparent strength is that non-residential projects take longer to complete, it takes longer to turn-off the spigot to use a familiar phrase.

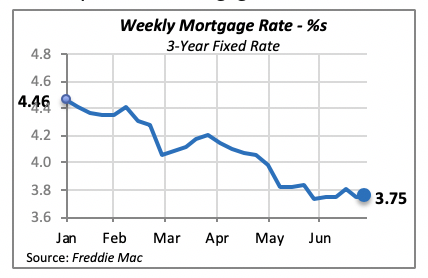

Mortgage rates declined last week

The 30-year fixed mortgage rate remained unchanged at 3.75%.

Note that this rate reflects the charges for loans issued the week before last, that is the week ended on July 27th. This is a few days before the latest policy move by the Federal Reserve Bank (FED), that on July 31st agreed to lower the federal funds rate by one-quarter point.

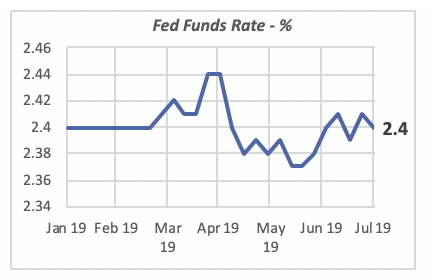

Now, in reality the FED does not target a specific value but rather a range. Currently, it has lowered the target for the federal funds from 2.00% to 2.25%; this is down from a 2.25% to 2.50% previously.

The chart below displays the weekly federal funds rate for the last six months, i.e. beginning of the year. The trading desk at the New York Fed manages the FED’s portfolio of Treasury bills, and buys and sells them as needed to maintain the rate between the target range.

Given the change in policy mentioned above, we should see the fed funds rate falling to fit into the new target range.

Manuel Gutierrez, Consulting Economist to NKBA

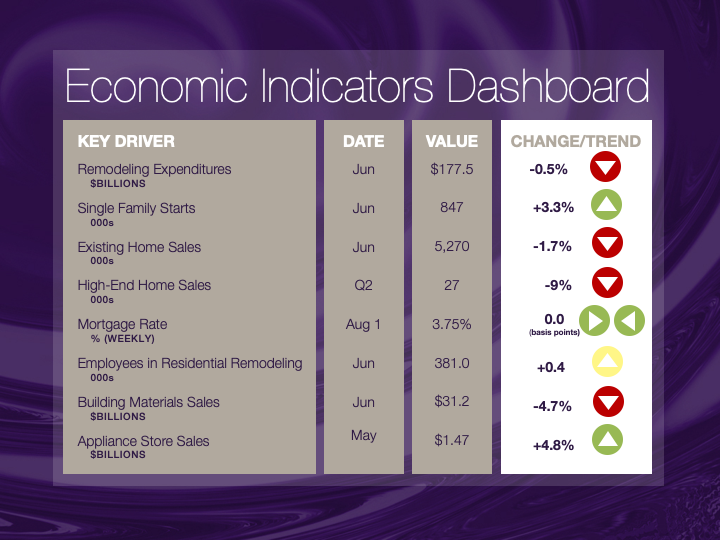

Explanation of NKBA’s Economic Indicators Dashboard

The dashboard displays the latest value of each economic indicator with a colored triangle that highlights visually the recent trend for each of the drivers. “Green” is a positive signal indicating that the latest value is improving; “Yellow,” as it’s common understood denotes caution because the variable maybe changing direction; and “Red” indicates that the variable in question is declining, both in its current value and in relation to the recent past.

Note that all the data, except for “mortgage rate” and “appliance store sales” are seasonally adjusted and are represented at annual rates.

Remodeling Expenditures. This is the amount of money spent on home improvement projects during the month in question. It covers all work done for privately-owned homes (excludes rentals, etc.). The data are in billions of dollars and are issued monthly by the U.S. Department of Commerce.

Single Family Starts. It is the number of single family houses for which construction was started in the given month. The data are in thousands of houses and are issued monthly by the U.S. Department of Commerce.

Existing Home Sales. These data are issued monthly by the National Association of Realtors, and capture the number of existing homes that were sold in the previous month.

High-End Home Sales. This series are sales of new homes priced at $500,000 and over. The data are released quarterly by the U.S. Department of Commerce, and are not seasonally adjusted. Thus a valid comparison is made to the same quarter of prior year.

Mortgage Rate. We have chosen the rate on 30-year conventional loans that is issued by the Federal Home Loan Mortgage Corporation (known popularly as Freddie Mac.) Although there are a large number of mortgage instruments available to consumers, this one is still the most commonly used.

Employees in Residential Remodeling. This indicator denotes the number of individuals employed in construction firms that do mostly residential remodeling work.

Building Materials Sales. These data, released monthly by the Department of Commerce, capture the total sales of building materials, regardless of whether consumers or contractors purchased them. However, we should caution that the data also includes sales to projects other than residential houses.

Appliance Store Sales. This driver captures the monthly sales of stores that sell mostly household appliances; the data are stated at an annual rate. We should not confuse this driver with total appliance sales, since they are sold by other types of stores such as Home Centers, for instance.

We hope that you find this dashboard useful as a general guide to the state of our industry. Please contact us if you would like to see further details.